The Whole Book

31 positions. $56,092. Every ticker, every gain, every kill vector. Free. Forever.

People keep asking what I actually own.

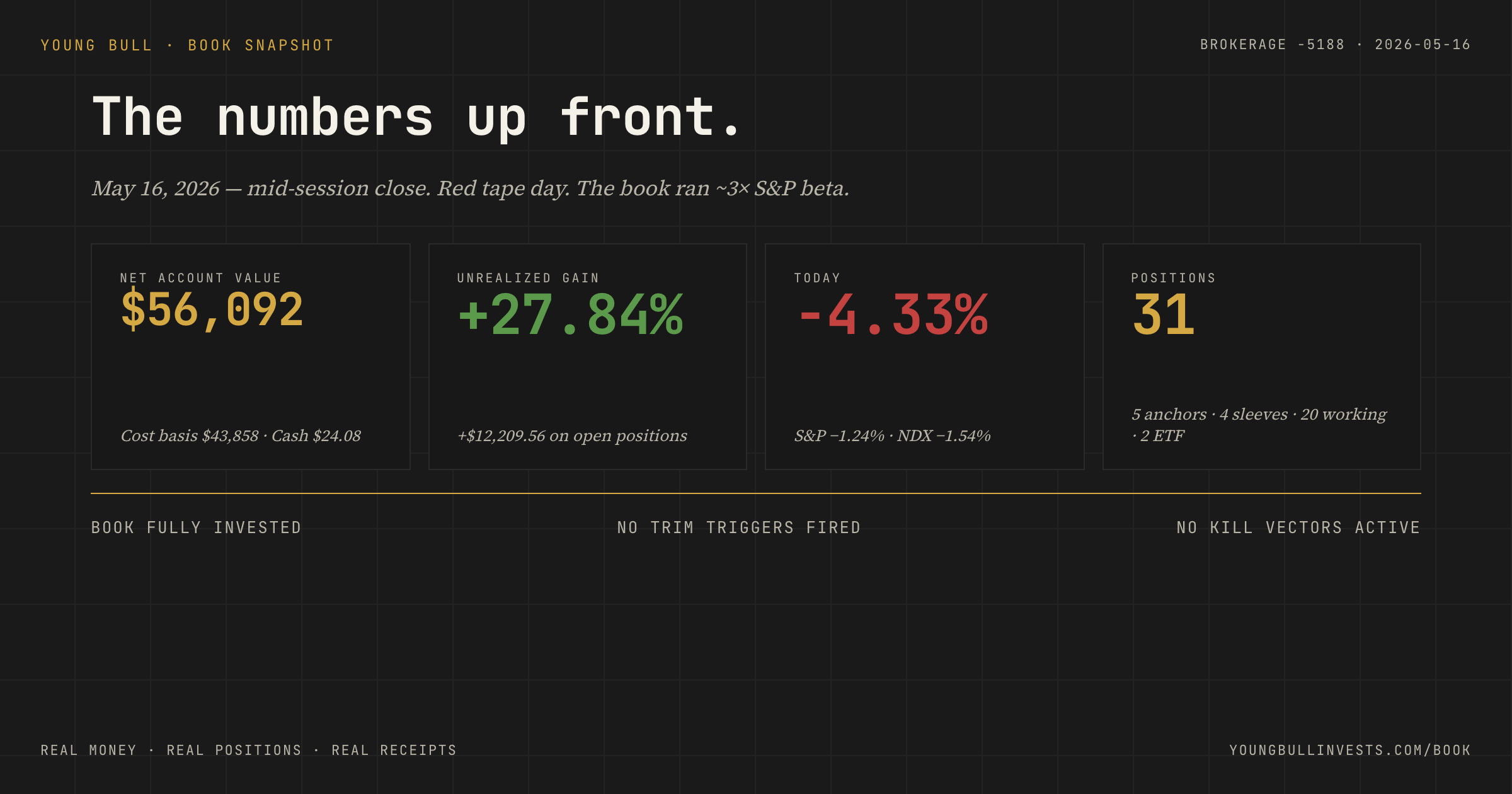

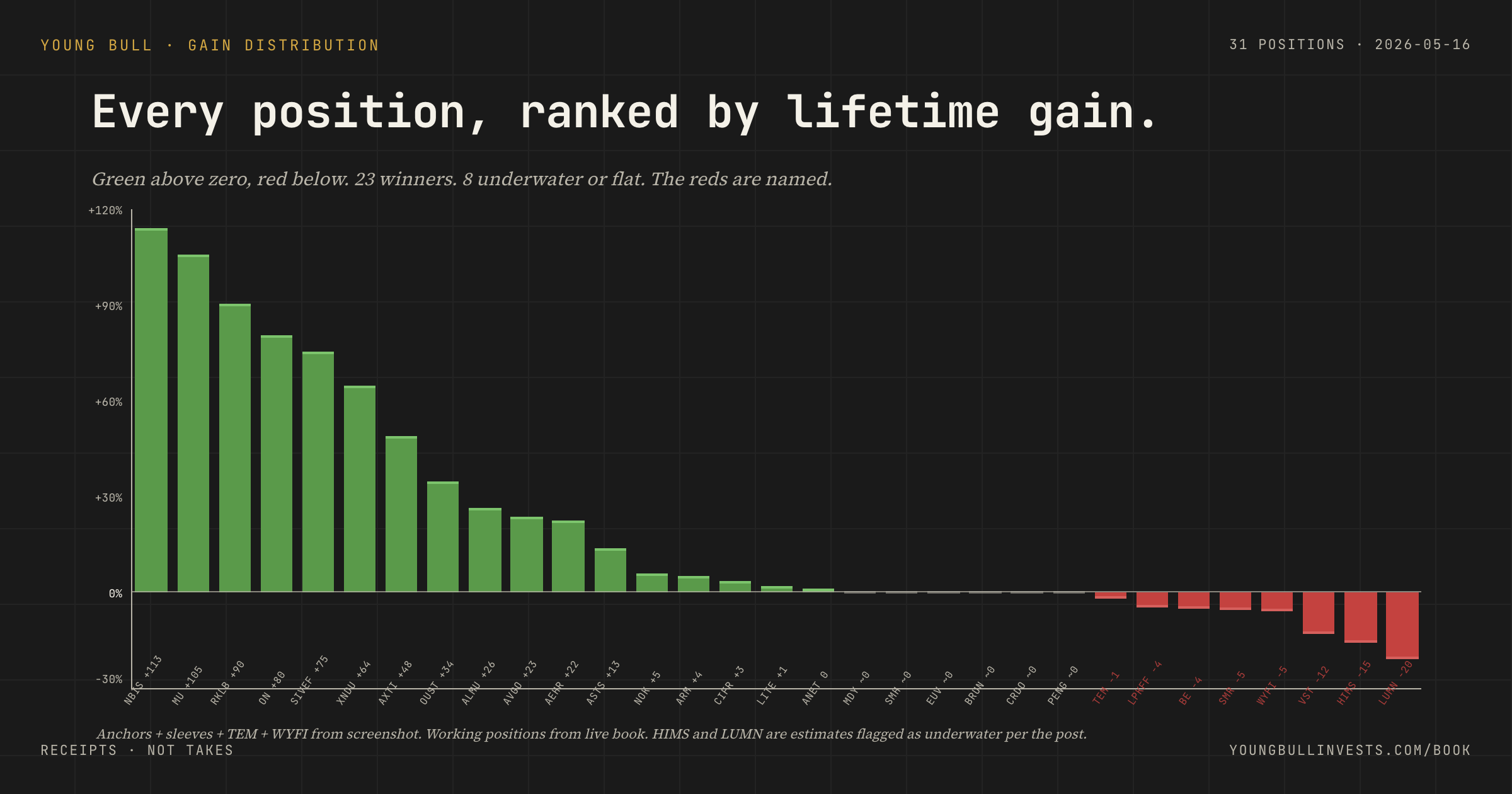

Here it is. The whole book. 31 positions. Net account value $56,092.27 as of the May 16 close. Up $12,209.56 lifetime, +27.84%. Real money. Real receipts.

I am starting deep dives on these names. Anchors first, then new adds and sells as they happen. The heavy per-position work goes behind the Pro paywall when Pro launches July 22. Before any of that lands, you should see the whole board.

One thing upfront. I am 17. I run real money against my own framework in public and I learn out loud. Some of these positions will work. Some will not. The whole book is the receipt of what I think. It is not a guarantee of what is right. Read it that way or get burned.

The promise has always been receipts before takes. This is the receipts page.

The numbers up front

Account value: $56,092.27

Cost basis: $43,858.63

Lifetime gain: +$12,209.56 (+27.84%)

Realized profit YTD: ~$9,000 (trim triggers and trades closed this year)

Cash: $24.08. Fully invested.

Position count: 31 (5 anchors, 4 high-conviction sleeves, 20 working, 2 ETF parking)

The book has been live the better part of this year. No kill vectors firing. No trim triggers firing. I am not adding here. I am writing this post.

Layer by layer

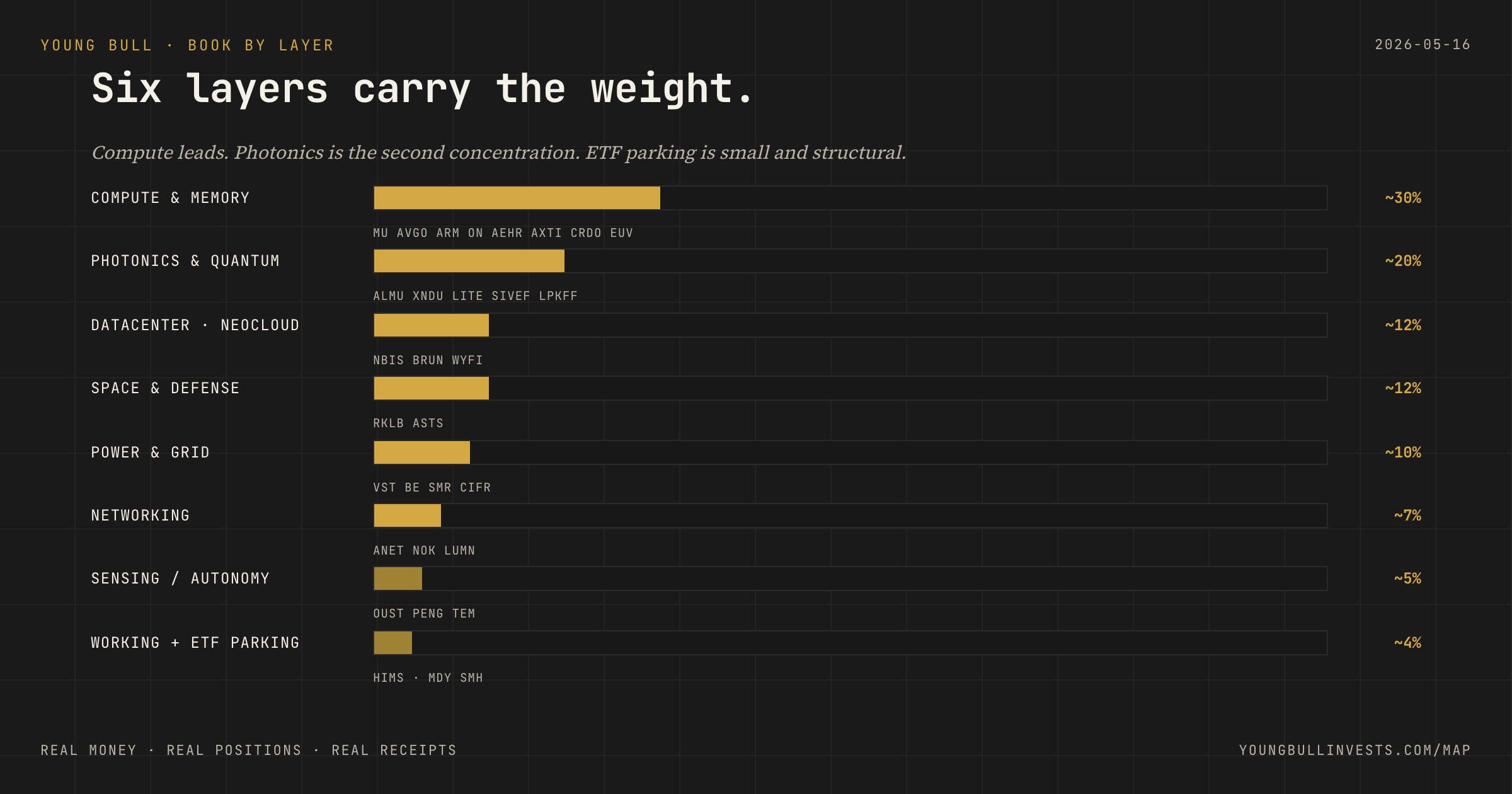

Compute & Memory ████████████ ~30% MU AVGO ARM ON AEHR AXTI CRDO EUV

Power & Grid ████ ~10% VST BE SMR CIFR

Datacenter / Cloud █████ ~12% NBIS BRUN WYFI

Networking ███ ~7% ANET NOK LUMN

Photonics & Quantum ████████ ~20% ALMU XNDU LITE SIVEF LPKFF

Space & Defense █████ ~12% RKLB ASTS

Sensing / Autonomy ██ ~5% OUST PENG TEM

Working / Honesty ██ ~2% HIMS

ETF parking ██ ~2% MDY SMHExact weights on the live book at youngbullinvests.com/book. Compute and memory is the heaviest by design. Every other layer feeds compute or routes its output. Photonics and quantum is second-largest because that is where I think the next mispricing lives.

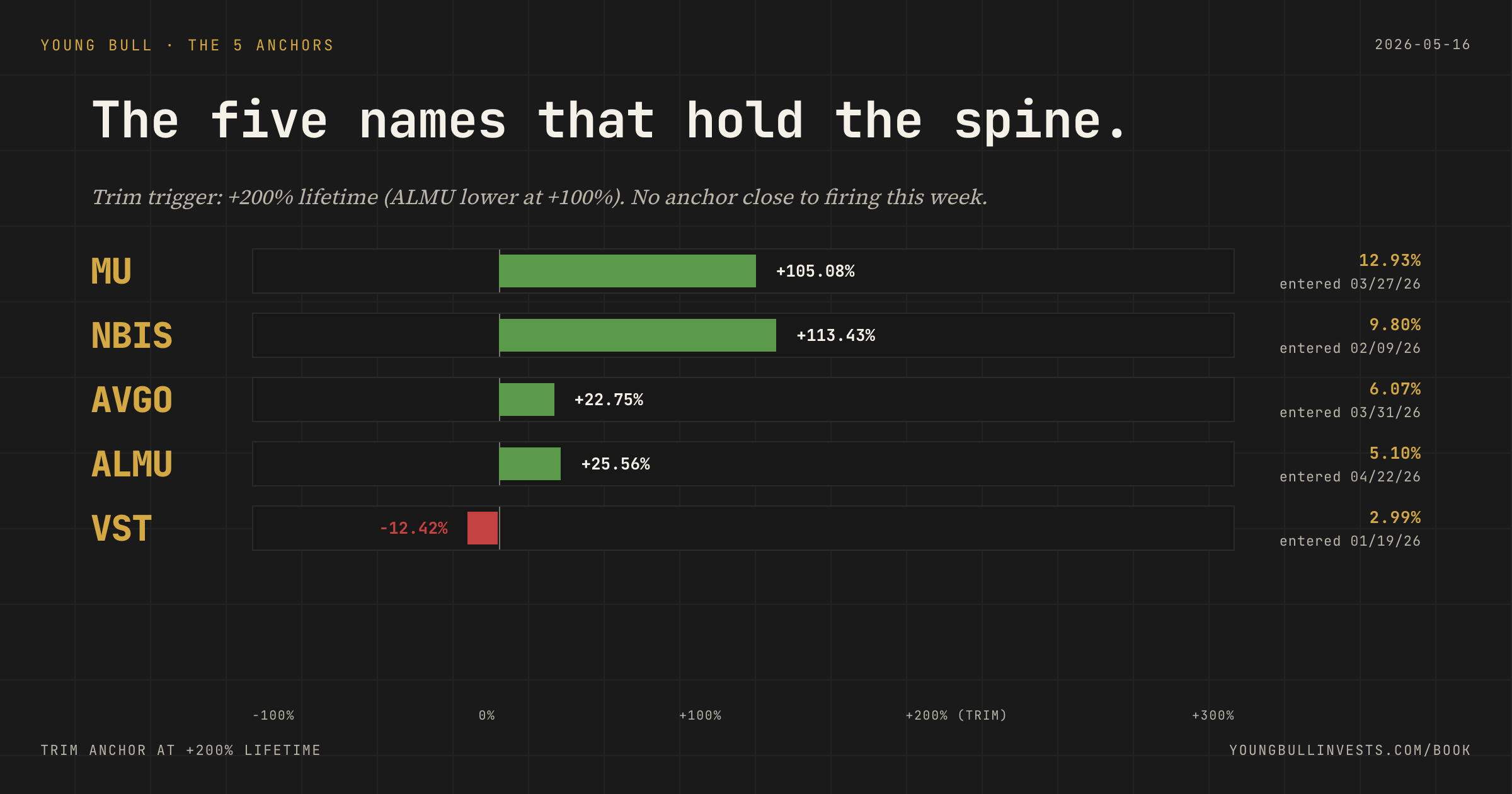

The 5 Anchors

The anchors are the spine. Five names. Five thesis floors I do not blink on. The trim trigger on every anchor is +200% lifetime (ALMU set lower at +100% because of smaller cap). I am not adding to anchors at these prices. I am not selling. I am letting the receipts compound.

MU. Micron Technology

Layer: Compute & Memory · Position: 12.93% (largest single) · Entry: 03/27/26 · Today: +105.08%

Why it is here. MU is the HBM trade. High Bandwidth Memory has been sold out before chips ship. Samsung and SK Hynix have signaled oversupply concern since February. Their February guide said HBM shortages last into 2027. SK Hynix already allocated its entire 2026 supply to NVIDIA. Customers are paying prepayments to lock 2027 allocation. Micron is the third leg of that stool, and the stock has done what a sold-out book does. The +105% lifetime is not a peak. It is what the cycle is paying right now.

Kill vector. Micron, Samsung, and SK Hynix would all have to guide oversupplied in the same quarter. Today all three guide undersupplied through 2027.

Trim trigger. +200% lifetime. 95 points away. Holding through any soft tape that does not break the supply-demand math.

Variant perception. Bears price MU off the historical DRAM cycle. Bulls price it off the AI-specific HBM cycle, where customers pre-pay for capacity that does not exist. Different cycle. Different math.

NBIS. Nebius Group

Layer: Datacenter / neocloud · Position: 9.80% · Entry: 02/09/26 · Today: +113.43%

Why it is here. NBIS is the cleanest pure-play on neocloud. AI compute infrastructure-as-a-service for hyperscalers and frontier labs. The Q1 2026 print (May 13): $399M revenue, +684% YoY, with the Nebius AI segment at $390M at 45% adjusted EBITDA margin. 2026 capex guide raised to $20-25B. A 1.2 GW Pennsylvania site is now on the page. The backlog is anchored by Meta ($27B, five-year) and Microsoft ($19.4B). Roughly $50B locked.

Kill vector. Hyperscaler concentration. Two customers carry the backlog. Either Meta or Microsoft pulling capacity in-house is the structural risk the Q1 print did not retire. The Eigen + Tavily + Clarifai acquisitions tell me Volozh is building the inference layer as back-door diversification, but customer concentration is not yet solved.

Trim trigger. +200% lifetime. 87 points away. Not adding into the post-print pop. Not chasing the gap.

Variant perception. Bears price NBIS as a capex burn. Bulls price it as a customer-prepayment-funded buildout with $9.3B liquidity and an asset-backed financing structure. Two P&L pictures, same balance sheet.

AVGO. Broadcom

Layer: Compute & Memory + Networking · Position: 6.07% · Entry: 03/31/26 · Today: +22.75%

Why it is here. AVGO is the only public name with a contracted custom-AI-silicon backlog at hyperscale. $73 billion of custom-silicon backlog with Google TPU, Meta MTIA, and OpenAI confirmed as customers. The networking side (Tomahawk and Jericho switching silicon) is the other half. Every hyperscale AI fabric in production runs on Broadcom switching silicon today.

Kill vector. Hyperscalers internalize the custom-silicon design. Google has Pixel Tensor and TPU. Meta has MTIA. The kill case is the next generation of custom AI chips moves off Broadcom's design service onto in-house silicon. Today the backlog says that is not happening on the timeline the bears price.

Trim trigger. +200% lifetime. 177 points away. Sized smaller than MU because the entry was late.

Variant perception. AVGO prints on both sides of the AI capex curve. Custom silicon goes up with training. Switching silicon goes up with inference. Most analysts pick one of those two lines. I own the company that owns both.

ALMU. Aeluma

Layer: Photonics & Quantum · Position: 5.10% · Entry: 04/22/26 · Today: +25.56%

Why it is here. ALMU is the smallest of the five anchors and the most asymmetric. Indium phosphide quantum-dot photonic ICs. Commercial laser shipping FY27. The thesis floor is the NASA award on April 21 for integrated quantum dot lasers, plus six government R&D contracts. The same photonic stack that builds AI datacenter optical transceivers builds the inter-satellite-link hardware in the orbital layer. One supply chain, two altitudes.

Kill vector. Execution. ALMU is pre-commercial-revenue at scale. The kill case is FY27 product slip past 2027 or a critical NASA program loss.

Trim trigger. +100% lifetime (lower than other anchors because of smaller cap). 74 points away. Adding more is off the table until the FY27 commercial revenue line.

Variant perception. Most photonics analysts cover ALMU as a venture-stage materials story. The bull case is to read the customer list. NASA. DoD. AI hyperscaler R&D groups. That is what rerates this name when the FY27 laser ships.

VST. Vistra Energy

Layer: Power & Grid · Position: 2.99% · Entry: 01/19/26 · Today: −12.42%. The worst anchor on the page.

Why it is here. VST runs the largest US nuclear fleet outside Constellation. Microsoft signed a 20-year PPA with VST for nuclear capacity. Meta did the same. Behind-the-meter nuclear is the only way certain hyperscaler workloads come online before 2030. The grid cannot deliver the megawatts hyperscalers have already contracted for (ERCOT has 226 GW of large-load requests in queue, three-quarters data-center demand). Nuclear capacity already built and already on the grid is irreplaceable. VST owns it.

Why it is red. Regulatory pendulum. The market punished the entire power-and-grid AI trade through April on natural-gas weakness, hyperscaler capex concern, and headline risk around behind-the-meter PPAs (the FERC review of Talen / Amazon spooked the cohort). VST got dragged even though the long-dated Microsoft and Meta PPAs are intact.

Kill vector. A regulator unwinds an existing behind-the-meter nuclear PPA on retroactive grounds. The headlines so far have been about new deals, not existing ones. Different bar.

Trim trigger. +200% lifetime. The trim rule does not apply when a position is red. The kill trigger has not fired. I am holding through this drawdown. This is the position that tests whether I run my own discipline rules in real time. I do.

Variant perception. Bears say nuclear is a regulated utility wrapped in an AI multiple. Bulls say nuclear is the only economically interconnectable base-load left, and the existing fleet is worth more than the comp set prices it. Twenty-year PPAs do not get unwound on a single regulator's tweet.

The 4 high-conviction sleeves

Done the work on, not promoted to anchor status. Sizing smaller. Conviction real.

ASTS. AST SpaceMobile

Layer: Space & Defense / Direct-to-cell · Position: 7.46% (second-largest after MU) · Today: +13.01%

This is my current vibe pick. The name I am leaning hardest into right now.

ASTS is the satellite direct-to-cell trade. Six BlueBirds in orbit (BlueBird 6 launched April 19 on Blue Origin's New Glenn). Target 45 by end of 2026. $3.5B cash. 60 MNO partners covering 3 billion subscribers globally. FirstNet authorization April 2025. T-Mobile direct-to-cell live across 500,000+ square miles at $10/user/month.

Q1 missed on revenue (60% miss, $14.7M vs $36.6M expected). FY 2026 guide reaffirmed at $150-200M. Back-half loaded by design. Calendarization story. Not a thesis break.

I added 10 shares mid-April on the BlueBird 7 failed-insertion drawdown. Position is back in the green. The lean: operational ramp visible, cash runway real, carrier ecosystem the moat. Next four quarters are about converting 60 MNO partners into revenue.

Kill vector. BlueBird operational failure or MNO revenue not appearing by Q4 2026.

XNDU. Xanadu Quantum Technologies

Layer: Photonics & Quantum · Position: 6.06% · Today: +64.04%

This is the name everyone in my circle already knows.

XNDU is the only public photonic-quantum pure-play. Room-temperature qubits on fiber. DARPA, Lockheed, AMD on the customer list. Five-year thesis.

The honest receipt: the +64% lifetime is the post-dilution number. The S-1 resale that hit May 5 crashed the stock −63% in 48 hours and reset the lifetime gain from a peak of +335% down to roughly +62%. The Xanadu + EVG manufacturing partnership announced the same week is what is keeping the thesis floor intact.

I trimmed XNDU once already (83 shares on April 15 at $25.22, $2,094 realized). Position now at the sleeve-rules-compliant size. Never full exit on XNDU. The discipline rule is in the playbook. This is the conviction moonshot.

Kill vector. A second dilution event before the manufacturing partnership produces commercial revenue.

BE. Bloom Energy

Layer: Power & Grid · Position: 4.92% · Today: −4.29%

This is the safe play.

BE makes solid-oxide fuel cells. Behind-the-meter power generation for data centers that cannot wait three years for substation interconnection. Same thesis as VST. The grid is the bottleneck. BE attacks it from the on-site generation angle instead of existing base-load.

I doubled the position on May 5 on a drawdown. Equinix already runs Bloom at scale. The receipts I am watching: hyperscaler announcements using Bloom for primary or backup AI datacenter power. The question is whether the AI-specific cycle accelerates the order book.

Kill vector. Hydrogen-economy unit economics break. Bloom's pivot to hydrogen is the long-dated lever. If green hydrogen costs do not fall on schedule, the multiple compresses.

LITE. Lumentum Holdings

Layer: Photonics (terrestrial + orbital crossover) · Position: 3.46% · Today: +1.23%

This one is backed by the deepest NotebookLM-sourced research in the book.

Lumentum builds the optical components for both AI datacenter transceivers and (per the Orbit thesis) the inter-satellite-link photonic stack going to orbit. Same indium-phosphide supply chain. Same coherent modulation. Different altitude.

Near-flat lifetime because the entry was recent and the optical-component cycle has been choppy on China-channel concerns. Structural thesis intact. Every hyperscaler optical transceiver upgrade goes through Lumentum or a Lumentum-adjacent vendor.

Kill vector. A coherent-modulation packaging shift that bypasses Lumentum's IP. Today there is no credible alternative.

The rest, by layer

Working positions. Smaller sizing, variable conviction, tighter kill vectors. The book is alive. The bench is not a museum.

Chips bench

ARM. IP royalty on every chip. Q4 FY26 record $1.49B. v9 royalty moving 25% → 60-70%. Deep dive May 12.

ON. SiC power for datacenters and EVs. Green.

AEHR. SiC burn-in test. Bull case: SiC capacity coming online 2026-2027 needs Aehr-class volumes.

AXTI. Compound semi substrates (InP, GaAs). Cross-pollinates ALMU.

CRDO. High-speed AI datacenter connectivity. AEC line is SerDes-adjacent.

EUV. Corgi's new ETF (May 6). EUV-litho / semicap-photonics supply chain. 41 holdings. Tiny starter.

Power & Grid bench

SMR. NuScale. First NRC-approved SMR. DOE backstop on Idaho. Pre-revenue, regulatory moat real.

CIFR. Cipher Mining. BTC miner pivoting grid interconnect to AI datacenter buildout.

Networking bench

ANET. Datacenter switching. Q1 +35.1% YoY, AI guide $3.5B doubling. CEO Ullal on the call: "our demand is actually the best I have ever seen in my Arista tenure." Bought the margin-flush dip.

NOK. AI optical pivot finally printing. Q1 AI/cloud revenue +49% YoY. Optical Networks +20%. Network Infra guide raised 12-14%. Infinera integrating. Argus upgraded to Buy. Holding through the re-rate.

LUMN. Fiber infrastructure. Position underwater. Dark-fiber asset thesis hasn't played out. Small, holding, would not add today.

Photonics & Quantum bench

SIVEF. Sivers Photonics. Indium phosphide adjacency. Small base, lifetime positive.

LPKFF. LPKF Laser & Electronics. German photonics laser equipment. Recent buy near breakeven.

Space & Defense bench

RKLB. Rocket Lab. Q1 $200M revenue, +63.5% YoY. 31 launch contracts signed in Q1 alone. Backlog $2.2B. Neutron debut Q4 2026. Mynaric acquisition puts RKLB in the photonic-orbital stack. Already trimmed at +100% per Adjacent Tech rules.

Sensing & Autonomy bench

OUST. Ouster. Lidar and perception. Position held.

PENG. Penguin Solutions. AI infra for tier-2 enterprises. The "every AI data center that is not a hyperscaler" trade.

TEM. Tempus AI. Q1 $348.1M, +36.1% YoY. Insights +44.1% on pharma. Six $100M+ partners on a 500-petabyte database. FY26 guide $1.59-1.60B. Variant: market reads Tempus as precision-oncology lab. I read it as the AI training-data layer for healthcare.

Datacenter / Neocloud small-cap bench

BRUN. Boost Run. Just-IPO'd neocloud (Nasdaq May 11, via Willow Lane SPAC). $940M contracted revenue at IPO. Targeting $375M+ ARR by FY2026 end. Pairs with NBIS at different scale.

WYFI. WhiteFiber. AI/HPC colocation + cloud. Recent IPO. −5.16%. Same thesis as BRUN, different angle. Kill vector: first full-quarter print missing on utilization or contract velocity.

Working positions

HIMS. Telehealth + GLP-1 distribution. Position underwater. Channel is real. Multiple compressed. Holding small, not adding.

ETF parking

On the watchlist

Same rigor as held positions, not bought yet.

HLIT. Pure-play broadband-edge networking. Q1 +43% YoY, backlog +87%, FY26 raised.

COHR. Photonics + laser systems. Deeper portfolio overlap with ALMU and LITE.

ONTO. Chip inspection and metrology. Semicap layer beneath ASML.

MTSI. High-perf analog/RF for AI datacenter, aerospace, defense. Overlaps CRDO.

NVT. Busbars, enclosures, thermal. Unsexy but load-bearing. Pairs with VST and BE.

VRT. Datacenter cooling and power. Classic AI-tailwind. 2026 prints tell whether entry waited too long.

None of these are buys today.

The questionable ones

Five positions are underwater: VST, BE, HIMS, LUMN, WYFI. Four covered above. The fifth (HIMS) is on the page because I want this list to include positions outside the Physical Layer thesis. GLP-1 channel intact. Multiple is not.

LUMN I would not enter today. Holding existing share count because the fiber-asset thesis is still on the page, but sizing is small enough it does not move the book.

Every newsletter that shows you only winners is doing a different job than the one I signed up for. You should see the red names. That is the receipt that matters.

How to read the book

Every ticker is clickable. Lands on the per-ticker research page (notes, kill vectors, trim triggers, latest agent runs).

The vote

Anchors first on the deep-dive queue. Tell me which one to write first:

MU. The HBM trade at +105% lifetime.

ALMU. The photonics + quantum laser anchor.

AVGO. Custom AI silicon + networking, both at once.

ASTS. The high-conviction sleeve I am leaning hardest on.

Drop the answer in the Substack poll above (or in the comments. Write-ins land in my notebook). Most-voted name gets written next.

The closer

Free: my book. Paid: the notebook.

The Substack stays free. The book page stays free. This post stays free.

Pro launches July 22 at $199/year. Founding 50 seats first. Pro is the per-position kill vector, trim trigger math, variant perception, NotebookLM audio briefings, and the Vestor agent watching your portfolio against mine. That is the differentiator. "Quinn sees your book." Not the other way around.

I am 17. The runway is 50 years. The Physical Layer of AI is the build. The whole book is the receipts.

When I am wrong, the postmortem lands before the next deep dive. That is the deal.

You have the whole book now.

Real money. Real positions. Real receipts.

What do you know about this company and their products Cerebras?

I just went to your site... I think we should chat, lol. Amazing, AMAZING job