Everyone is staring at AI. AI is staring at space.

The bears think space is a meme, which is understandable when RKLB 0.00%↑ is trading like a rocketship, however that might not be the case here. The consensus thinks space is a 2030 story. The AI-obsessed think space is downstream of the rack. All three are wrong by the same mechanism. The pull is going both ways.

The terrestrial Physical Layer of AI is hitting real bottlenecks in 2026. HBM sold out through 2027. CoWoS booked through mid-2027. ERCOT has 226 gigawatts of large-load interconnection in queue. The supply response is starting to push capacity into orbit. That is the demand side.

At the same time, AI is the thing making the orbital extension economically viable. Constellations route themselves through reinforcement learning. Rocket engines are designed by AI before a single weld. Earth observation feeds the foundation-model training set. On-orbit inference is live and shipping today. That is the supply side.

I have been quietly positioned in that overlap for months. The book runs ALMU, RKLB, ASTS, plus adjacent photonics names that build the inter-satellite-link hardware on the ground. This piece is the thesis, with six new deep cuts.

The pull is two-way.

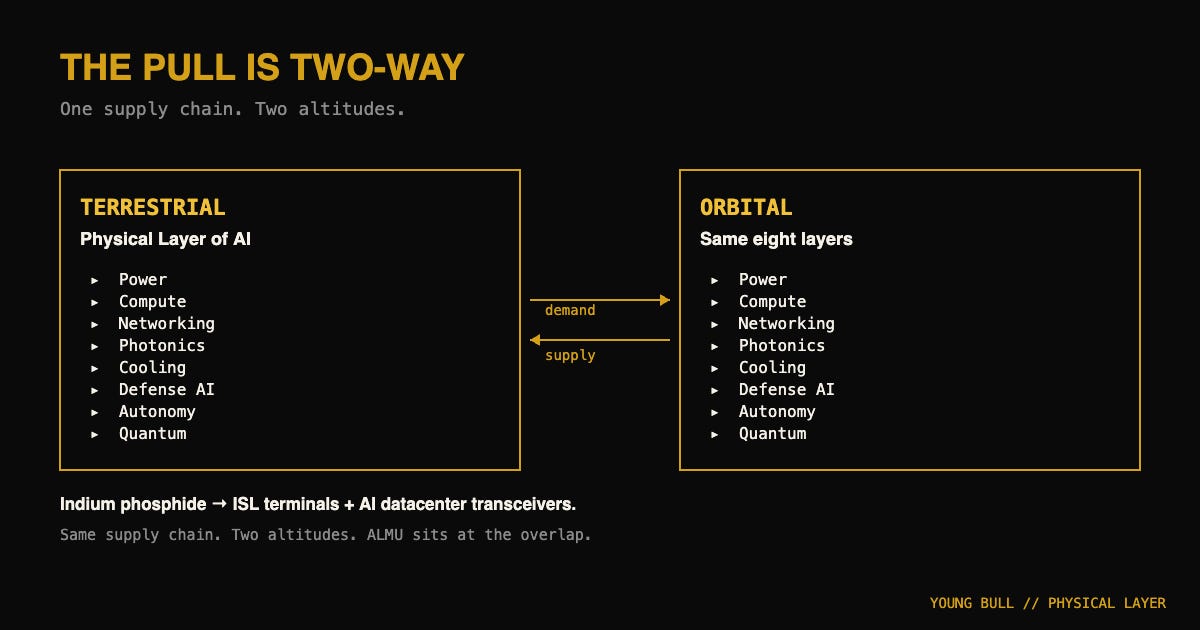

The orbital domain inherits all eight layers of the terrestrial Physical Layer. Constellations need power, compute, networking, photonics, cooling, defense AI, autonomy, and quantum. Same eight.

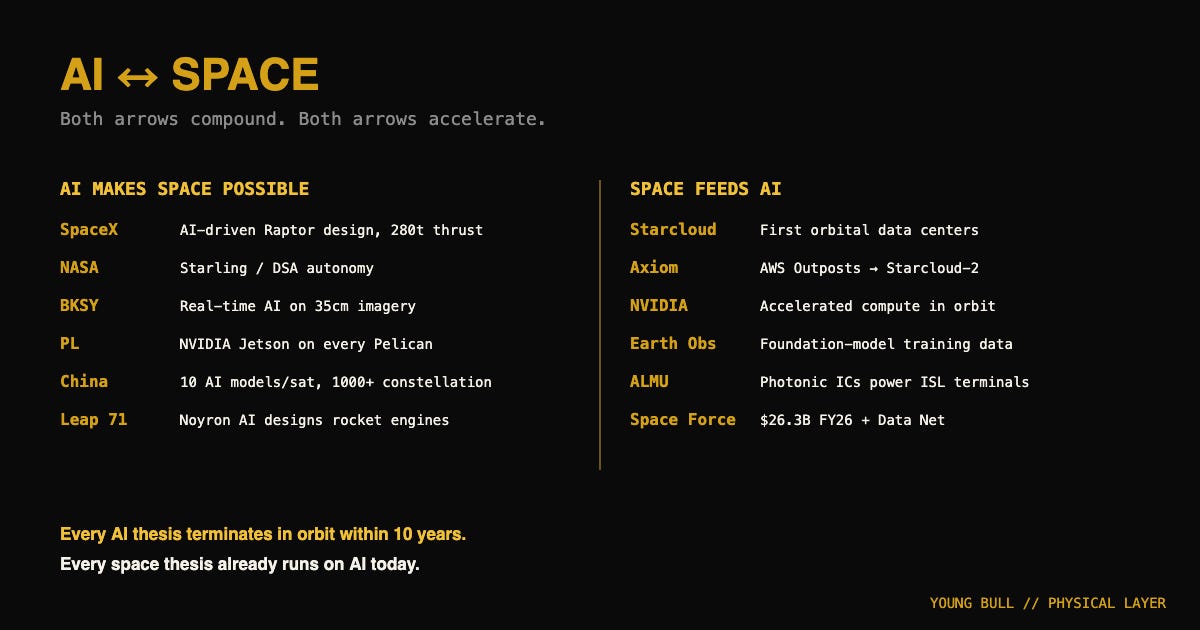

Starcloud and Axiom launched the first orbital data center nodes to low-Earth orbit on January 11, 2026. NVIDIA confirmed Aetherflux, Axiom Space, Kepler Communications, Planet Labs, Sophia Space, and Starcloud are running NVIDIA accelerated computing in orbit. Starcloud plans to deploy the first AWS Outposts hardware in space on Starcloud-2.

The interconnect between satellites is optical. Inter-satellite laser links (ISLs) use the same photonic integrated circuit stack as terrestrial AI datacenter optical transceivers. Same indium phosphide. Same coherent modulation. Same supply chain. ALMU sits at the front of this overlap. Indium phosphide quantum-dot photonic ICs are exactly the technology stack that powers next-generation ISL terminals.

One supply chain. Two altitudes.

AI is making space possible.

SpaceX uses AI to design Raptor. Engineers ran AI-driven simulations across thousands of design configurations before metal was cut. The latest Raptor delivers 280 tonnes of sea-level thrust. The same AI tooling drives heat-shield optimization, convex-optimization landing for Dragon, and the autopilot stack that brings boosters back to the chopsticks. Without AI in the loop, Starship cadence does not scale to 12 orbital tests in 2026 and Falcon 9 does not run 165 launches per year.

Constellations route themselves with AI. NASA Starling and Distributed Spacecraft Autonomy projects teach spacecraft to share data, divide tasks, and self-organize. Reinforcement learning agents optimize constellation scheduling and link management. AI and machine learning are not a future aspiration. They are the operational fabric that makes the buildout work today.

China just shipped a satellite constellation with 10 AI models per node. When the full deployment hits 1,000+ satellites, it is expected to perform 100 quintillion operations per second in orbit.

BKSY Gen-3 satellites do real-time AI analytics on 35-centimeter imagery before the data touches a ground station. The customer gets the inference result, not the raw pixels. PL ships NVIDIA Jetson on every Pelican. Compute on the bird, ship the result. Leap 71 Noyron AI autonomously designs rocket engines from physics constraints.

AI demand pulls the Physical Layer into orbit. AI capability makes the orbital extension cheap, fast, and autonomous enough that the buildout completes inside a decade rather than a generation.

Is space next? Is it now? Is it everything?

Three questions. Three answers.

Is space next? No. Space is now. SpaceX filed S-1 with the SEC on April 1, 2026. The roadshow is slated for June. RKLB printed $200 million in Q1 revenue. ASTS launched its sixth BlueBird on Blue Origin’s New Glenn. Starcloud put two orbital data center nodes in LEO in January. Starlink crossed 10 million subscribers in February. T-Mobile direct-to-cell is commercially live across 500,000+ square miles. None of these are future-tense.

Is it everything? It is becoming everything, on a multi-year clock. The space economy is forecast at $1.8 trillion by 2035 (McKinsey + WEF). Space Force is requesting $26.3 billion in FY26 and signaling $1.5 billion for the Space Data Network in FY27. Every Physical Layer name in my book has a plausible orbital revenue line by 2030.

Was space next? Yes. The question is now obsolete. The buildout is already in motion.

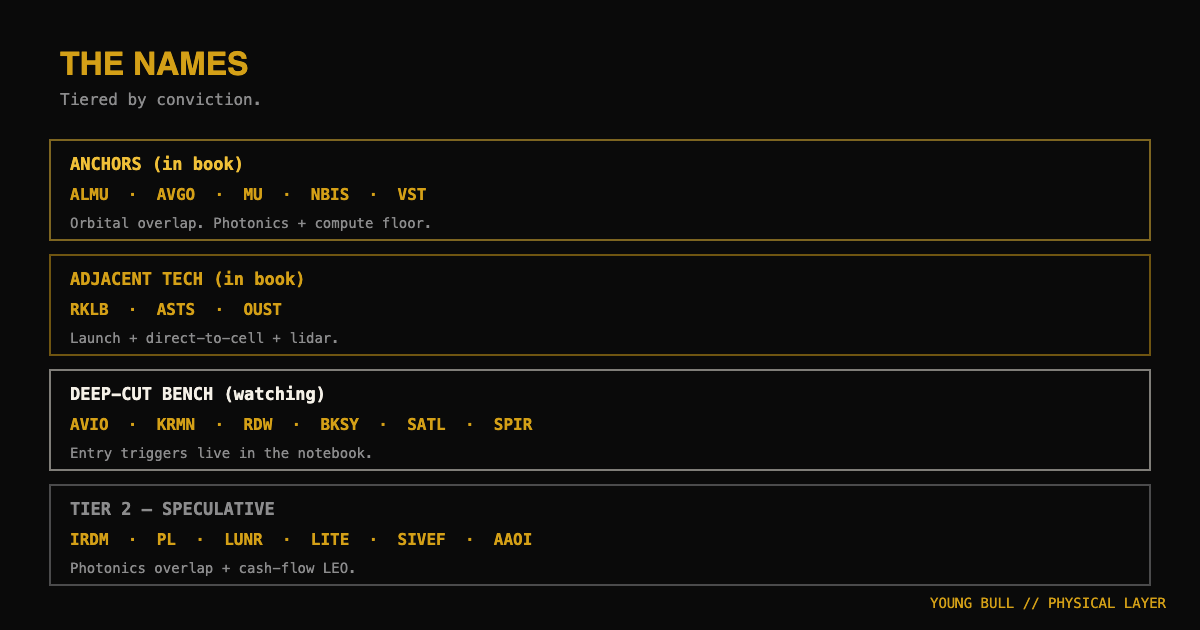

The names, tiered by conviction.

Anchors with orbital overlap (in the book)

ALMU. Photonics. Indium phosphide quantum-dot photonic ICs. NASA award 4/21 plus six government R&D contracts is the floor. The same supply chain that builds AI datacenter optical transceivers also builds satellite ISL terminals. Positioned for both.

AVGO. Compute IP plus networking. $73 billion custom AI silicon backlog. Naturally extends to satellite-grade processors as on-orbit compute scales.

MU, NBIS, VST. The other anchors benefit indirectly from the SpaceX IPO sentiment lift but the orbital thesis does not change their scope.

Adjacent Tech sleeve (in the book)

RKLB. Q1 2026 revenue $200.3 million (+63.5%). Backlog $2.2 billion. 31 launch contracts signed in Q1 alone, more than all of 2025. Neutron debut targeted Q4 2026. Electron 21 of 21 in 2025 at 100% success. The Mynaric acquisition puts RKLB directly in the photonic interconnect layer. Position significantly positive lifetime. Trimmed at +100% per discipline.

ASTS. Targeting 45 BlueBirds by end of 2026. BlueBird 6 launched April 19, 2026. $3.5 billion cash, 60 MNO partners covering 3 billion subscribers. FirstNet authorization 4/25. Underwater currently. Holding through the operational ramp.

OUST. Lidar and perception. Autonomy crossover.

Deep-cut bench (watching, not yet positioned)

AVIO. Italian launch. Vega-C transition from Arianespace finalized December 2025. 9M 2025 revenue +26%. Backlog €1.86 billion. Defense propulsion heading to 50% of revenue. The European launch + missile dual-use prime independent of Boeing/Airbus politics.

KRMN. Karman Holdings. IPO Feb 13, 2025 at $22, opened +30%. $581.9 million raised. Thousands of components on Orion + SLS since program inception. The picks-and-shovels inside defense-space modernization.

RDW. Redwire. FY26 guide $450 to $500 million. Six ROSA arrays on the ISS. Building ROSA for NASA’s Lunar Gateway + Astrobotic’s Lunar Vertical Solar Array. The orbital infrastructure pure-play.

BKSY. BlackSky. Four Gen-3 satellites delivering 35cm imagery with real-time AI analytics built in. FY26 $130 to $150 million. The closest pure-play on AI-enables-space. Customer pays for the answer, not the data.

SATL. Satellogic. Q1 +80% revenue. $121.9M cash, first positive operating cash flow. Sovereign-data play. Defense customers worldwide need their own EO.

SPIR. Spire Global. 110+ CubeSats on orbit. FY26 $75-85M guide (+50% ex-maritime). Weather + RF data play.

Tier 2, photonics overlap, speculative

IRDM cash-flow LEO machine. PL Bloomberg of Earth Data. LUNR lunar economy. LMT, RTX, NOC primes with space inside. LITE, SIVEF, AAOI on the photonics supply chain. SPCE, HOLO, UFO, ARKX acknowledged, not entering.

Skin in the program.

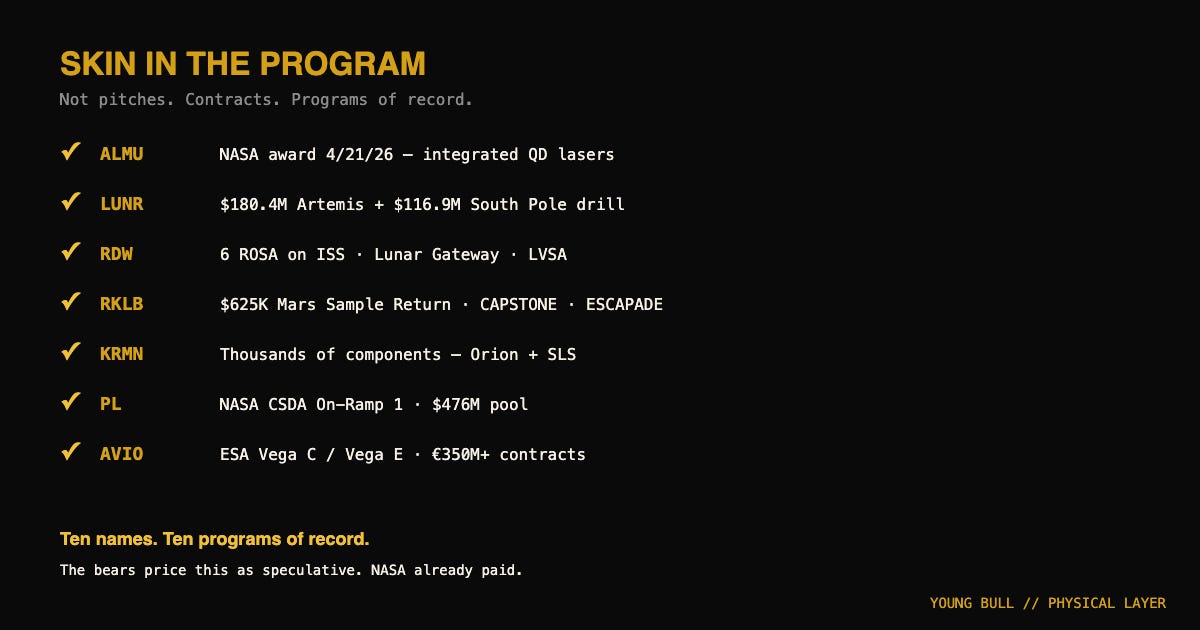

Every name in this piece has a NASA or ESA contract on the books. Not press releases. Not pitches. Contracts.

ALMU. NASA award April 21, 2026 for integrated quantum dot lasers. Non-dilutive funding. On-chip QD lasers for silicon photonics, AI datacenter interconnect, defense, aerospace, quantum. The bridge between the AI book and the orbital thesis is now an explicit NASA program of record. I own ALMU. The NASA program is part of the thesis floor.

LUNR. NASA CLPS prime on the Artemis program. $180.4M for Artemis science delivery. $116.9M for the South Pole drill mission. Near Space Network contract up to $4.82 billion. IM-1 (Odysseus) landed February 2024, the first private moon landing.

RDW. Six Roll-Out Solar Arrays on the ISS today (+20-30% power). Building ROSA for NASA’s Lunar Gateway PPE + Astrobotic LVSA. NASA on the ISS. NASA on the Gateway. NASA on the lunar surface.

RKLB. $625K Mars Sample Return study contract. CAPSTONE delivered for Lunar Gateway orbit test. ESCAPADE twin Photons now in Mars science operations. Solar cells supplied for Artemis II Orion.

KRMN. Thousands of components for Orion and SLS since program inception. Hatch release mechanisms, pressure-vessel hardware, isogrid panels, propellant tanks. KRMN is on the Artemis hardware sheet at the metal level.

PL. NASA CSDA On-Ramp 1 Multiple Award through November 15, 2028. $476 million cumulative pool. PlanetScope to 300,000+ NASA scientists. BKSY, SATL, SPIR are also on the same On-Ramp 1 pool.

AVIO. ESA prime for Vega C / Vega E. €350+ million in ESA contracts. The European launch partner that complements the American stack.

Ten names. Ten programs of record. The space economy the bears price as speculative is the same space economy NASA procurement has already paid for.

What the bears miss.

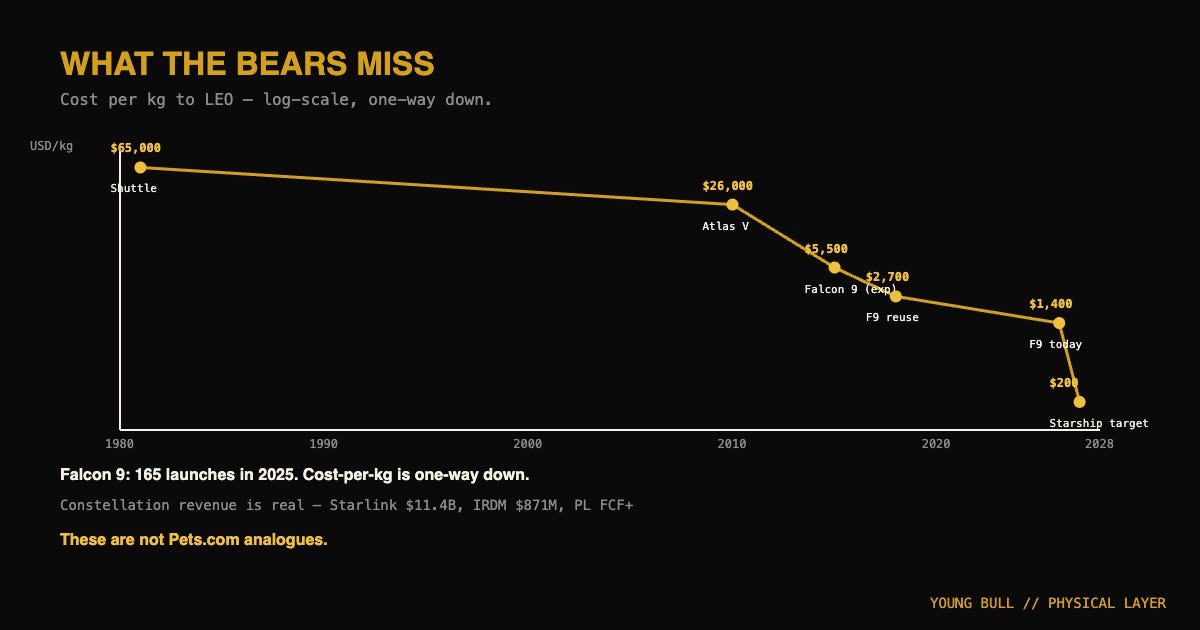

Launch economics changed permanently in 2025. Falcon 9 reusability is the baseline. 165 launches in 2025. Cost-per-kg trajectory is one-way down. The platform is real.

Constellation revenue is real, not speculative. Starlink $11.4 billion in 2025. IRDM $871 million with $318 million FCF guided. PL profitable on FCF. RKLB Q1 $200M record. These are not Pets.com analogues.

Defense spending is structural. Space Force $26.3 billion FY26. China is building its own constellation. Multi-year authorization.

The biggest miss is the AI piece. Bears who write off space as cyclical are reading a 2020 chart, not a 2026 one. AI demand pulls the Physical Layer into orbit. AI capability makes the orbital extension economically feasible. Both arrows accelerate each other.

The book and the decision tree.

ALMU anchor. Position lifetime positive. Trim trigger at +100%. RKLB Adjacent Tech, significantly positive lifetime, trimmed at +100%, not adding. ASTS Adjacent Tech, currently red, holding through the BlueBird ramp. The other four anchors (MU, NBIS, AVGO, VST) are terrestrial Physical Layer.

Deep-cut bench (AVIO, KRMN, RDW, BKSY, SATL, SPIR) is watching with thesis depth. Entry triggers live in the notebook.

If SpaceX prices the IPO above $1.5 trillion, expect a sentiment rally across the entire complex. Not adding into the rally. Discipline applies. If SpaceX prices below $1 trillion, expect a flush. RKLB could see the 30-40% pullback that triggers reentry consideration.

Privacy frame stays. Percentages only. No shares, no cost basis, no per-position dollar values. The position-level reasoning lives in the notebook.

The Pro hook.

Free: my book. Paid: the notebook.

Pro launches July 22, 2026, at $199 per year. Kill vectors per ticker. Trim triggers. Decision-tree updates inside 24 hours of major events. Deep-cut bench tracking with entry thresholds. The Vestor agent watches subscriber portfolios and surfaces what crosses with mine.

Founding 50 seats fill first.

The closer.

Every AI thesis terminates in orbit within 10 years. Every space thesis already runs on AI today. The names that build the datacenter are the same names that build the constellation. The pull is going both ways.

I am 17. The compound runway is 50 years. The Physical Layer of AI is the build. Orbit is the layer where AI starts to manage itself.

I am positioned.

Real money. Real positions. Real receipts.